Why business at London’s specialty-insurance hub has surged

Its high profits will not last forever, but it will remain a global leader for specialist cover

Shipping is not the safest industry—just ask any oil-tanker captain in the Persian Gulf. That’s why gatherers at Edward Lloyd’s coffee house in London, from around 1688, decided to share the financial risk for the hairiest seafaring ventures. More than three centuries later, a shipowner wanting to insure a vessel passing through the Strait of Hormuz is still likely to call on the city’s specialists for a quote.

Data from the London Market Group (LMG), a trade body, showed that London’s wider specialty-insurance and reinsurance market supported 61,000 jobs in 2024. The Lloyd’s of London marketplace, a descendant of the old café, makes up around 40% of that $187bn business, and now covers far more than just shipping. It wrote nearly £60bn-worth ($81bn) of contracts in 2025, doubling in real terms since 2015.

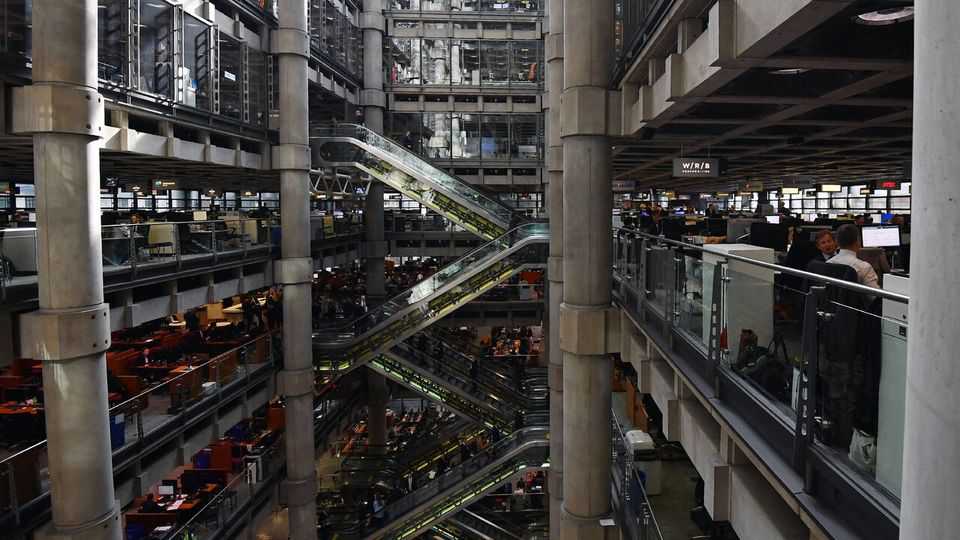

One of its strengths is the concentration of specialists. Like its caffeine-dispensing Stuart forebear, the Lloyd’s building in London serves as a meeting place. Today, it bustles with brokers and underwriting syndicates, which write policies and share risk. This structure promotes innovation. The first policies for a car, plane and satellite were written there. More recently, it has carved out a niche in cyber and energy-infrastructure insurance—and it has grown its share of the global marine, energy and property insurance markets. Interest in those areas recently prompted Zurich, a Swiss insurance giant, to acquire Beazley, a large underwriter.

Lloyd’s policies used to be exclusively backed by capital from wealthy individuals, or “Names”. By the 1970s their numbers were swelling rapidly. Monied aristocrats were joined by celebrities, politicians and upstart millionaires from the City. As it does now, Lloyd’s offered investors enticing tax breaks and the opportunity to make a handsome return on their capital. The catch was that they held unlimited liability for losses. After asbestosis-related claims struck in the 1990s thousands of Names lost money; many were ruined.

A slicker organisation has emerged since. Much of the capital now comes from insurers rather than landowning dilettantes. Some individuals still invest today, but mostly through “NameCos”—companies where liability is sensibly limited.

Investors have done well recently. Property insurance became especially lucrative. A run of disasters, beginning with a ruinous hurricane season in 2017, prompted insurers to raise prices. After 2022 catastrophes lightened. This helped make the past three years the most profitable in more than a decade (see chart). In 2025 pre-tax profits across the Lloyd’s syndicates were £10.6bn; the ten-year average is £2.5bn. The return on capital exceeded 20%.

Firms in other hubs have seen profits soar too. LMG’s data showed London’s growth has trailed that of Bermuda since 2020. But overall London’s share of the market has grown.

Now Lloyd’s is bracing as the insurance market starts to cool. In 2025 its prices fell for the first time in years. “Competition has come back a little bit more,” explains Emily Apple, a director at Alpha Insurance Analysts, a firm which invests in syndicates on behalf of members.

Lloyd’s boasts that it has paid out for even the most devastating claims, from the sinking of the Titanic to the attacks on the World Trade Centre and the war in Ukraine. The impact of the Iran war remains uncertain. No reports of major losses for marine insurers have surfaced yet, according to an analysis by Ms Apple’s firm. Shipping traffic halted after the fighting broke out and policies were rewritten at much higher prices, for which there were few takers. Some terrorism insurers have suffered losses, but demand has also gone up. Fear, after all, is good for business. ■